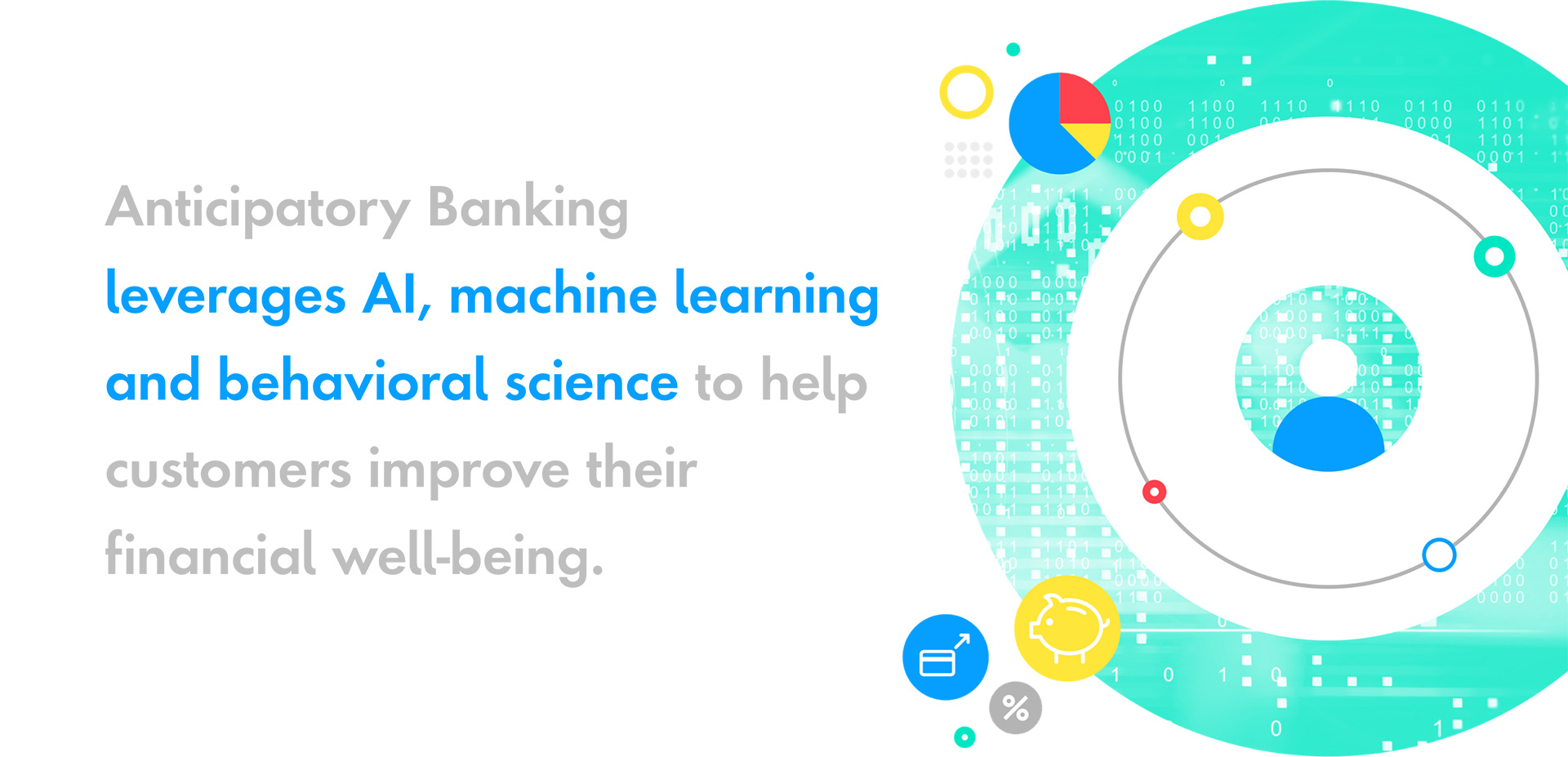

Turning challenges into opportunities

In today’s competitive environment, new market players, changing consumer behaviors and technology advances have created significant downward pressure on banks’ ability to grow, causing higher customer attrition rates and limiting banks’ ability to cross-sell products and services. But banks have a unique opportunity to leverage these trends to win over their customers and obtain new ones in the process, thereby creating top line growth.

Customer attrition

A typical global bank loses approximately 18 percent of an average balance to customer attrition. The reason? Banks are failing to offer customers what they truly want: lower rates and fees and better customer service. In fact, 40 percent of customers say they are willing to switch if these issues are not addressed.2 The key to stemming attrition will be to personalize experiences, giving customers exactly what they want. Without them, banks face losing customers at even higher rates.

Cross-sell and upsell

Many banks struggle with cross-selling and upselling for one simple reason: they aren’t able to deliver what their customers need, when they need it. The good news is that almost 90 percent of customers own a deposit account with a global retail and commercial bank, so they already have the customers in-house. It’s simply a matter of creating growth within their existing customer base by anticipating customer needs, and leveraging insights to determine their interest and wants. In doing so, banks can dramatically improve their cross-sell and upsell rates and increase overall customer engagement.

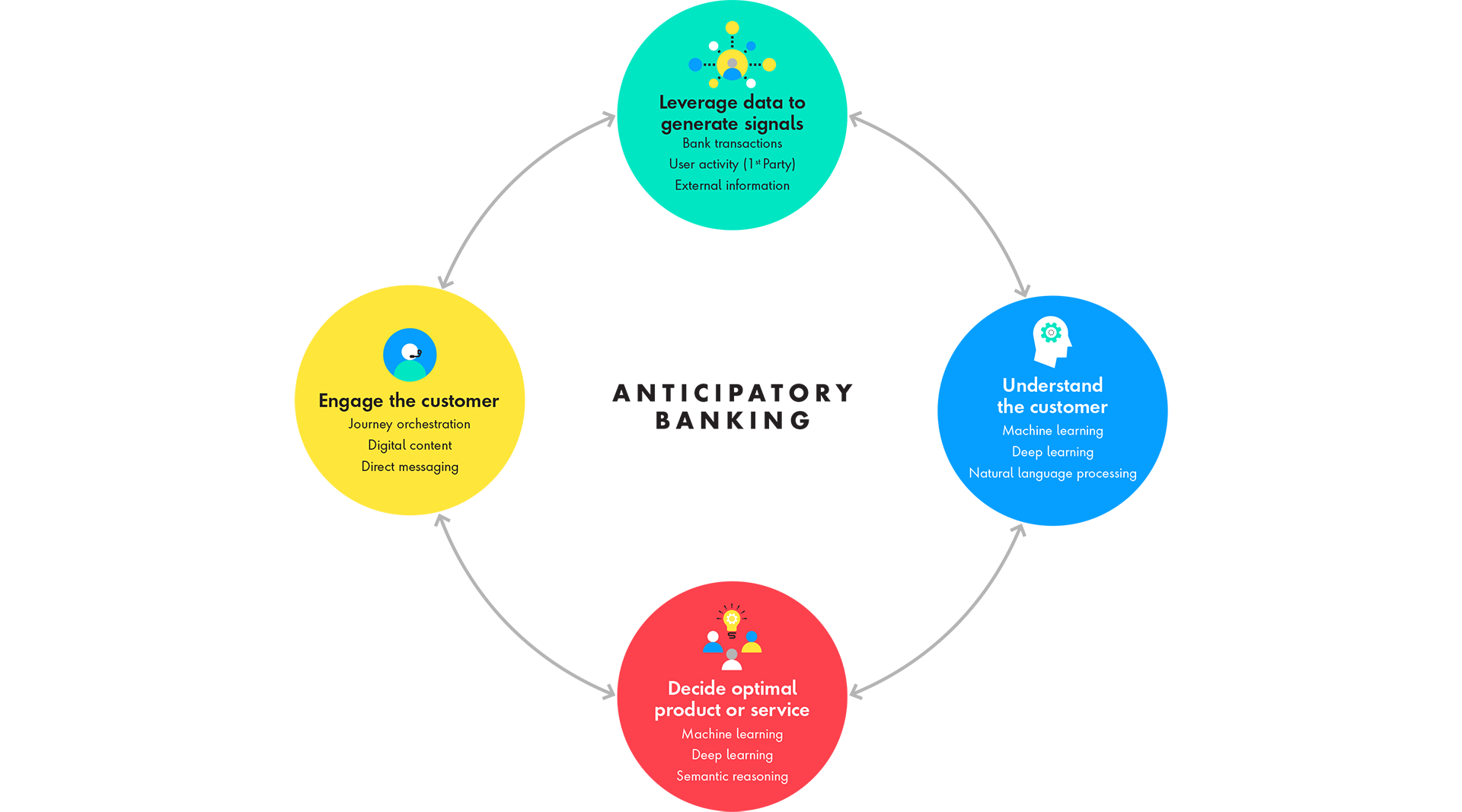

By better understanding and delivering on customer needs, banks can stem attrition and improve cross-sell and upsell efforts—increasing net interest income by an average of 190 bsp. Identifying where to focus within the business to drive growth may be the easiest piece of the puzzle. What concerns most bank executives today is not the “what” but the “how.”