Interview has been edited for style and clarity.

Q&A

Fuel Station 2025: Q&A with Iyad Ghanem on France

Even in a country where supermarkets are a major presence in fuel retail and regulations will ban the sale of gas-powered cars in a decade or two, big oil can save the fuel station.

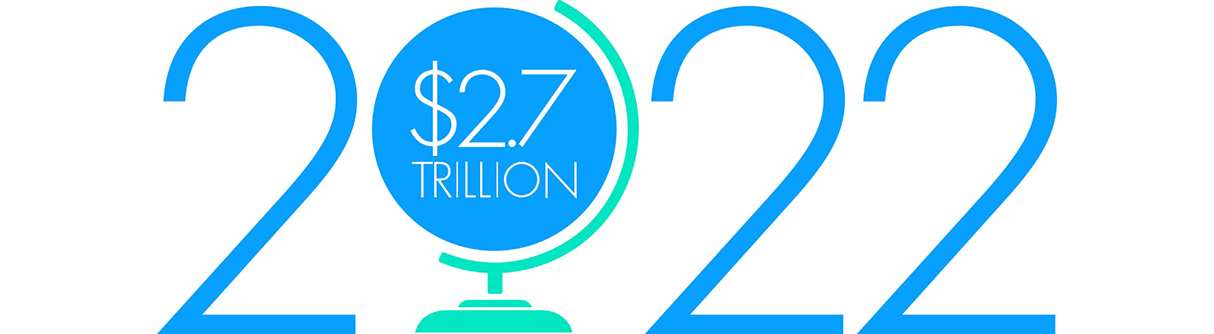

Are fuel stations dying? It’s a strange question to ask of a market that is expected to reach $2.7 trillion in revenue globally by 2022. But with the rise of alternative fuel sources, ride sharing, electronic vehicles and the impact of changing consumer behaviors and evolving regulations, the question is not so outlandish.

To explore what the fuel station will look like in 2025—and whether it will one day go the way of drive-in movie theaters and public telephone booths—we talked with Publicis Sapient energy and commodity experts in several geographies.

Iyad Ghanem, director, offered a view of the market in France. Over the past decade, the country has seen more than half of its fuel stations close, and retailers now own as many stations as the supermajors do. Ghanem’s perspective? Fuel stations aren’t dying. But they are on the road to being very different.

"...a market that is expected to reach $2.7 trillion in revenue globally by 2022."

What is unique about the French market?

The most unique characteristics come from historical trends and regulations. The presence of large supermarkets like Carrefour in fuel retail, which we see across western Europe, certainly shapes the competitive landscape here.

There is something that is specifically French too. The Multiannual Energy Programme is focused on reducing fossil fuel consumption and supporting the transition to more sustainable fuel sources. While other countries have regulations that aim for similar ambitions, the timelines and the constraints imposed are singular. By 2030, gas-powered vehicles will not be allowed in Paris. The energy transition to a low-carbon economy is the foundation of all the change we’re seeing in this space.

Electric vehicles are a major part of the story of the fuel station of the future.

Absolutely. While the size of the electric vehicle market in France, and across Europe for that matter, is still less than one or two percent, the growth we’re seeing is phenomenal.

France saw a 46 percent increase in electric vehicle sales just in the first half of 2019.

There is strong momentum here. In response, oil and gas companies have already begun to direct CapEx into the electric vehicle play. The goal is to position themselves in the right place in the value chain to extract the value from electric vehicle charging. They want to avoid being forced into a commodity play.

But the addition of charging stations in fuel stations has a far-reaching impact that the industry cannot leave unanswered. Charging a car takes a lot more time than filling up the tank does—about 15 minutes with today’s technology. This means that consumers will start spending more time at fuel stations, which has profound implications for the customer experience.

The customer experience must change. Consumers will want different things. It will take new kinds of service experiences for companies to stay relevant and build brand loyalty. Price and proximity won’t necessarily be the most powerful draws anymore. To understand the future consumer, traditional players need to shift their perspective from being a fuel supply business to being a retail business that sells fuel.

This mindset shift opens breakthrough possibilities around customer experience. Technology will be an enabler. Think about connected cars, for example. More of them on the road in the next five years. They will be fitted with GPS and advanced smart technologies that not only tell drivers they are low on gas, but direct them to the station they should stop at based on their route and other unique parameters. The technology will take a better part of the value chain, and energy players need to be in this space too.

Cars won’t always make the decision about where to stop for gas in the future, will they?

Don’t worry, drivers won’t lose their autonomy. The point is that they will have more tools at their fingertips to make educated choices. The fuel stations that offer the experiences that customers want will have the advantage.

But the ideal experience means different things to different people. Some people want to pull in, pump and pay and manage their account seamlessly in an Uber-inspired, app-centered experience. Others are interested in convenient retail experiences. The trick for the industry is to use data to get a very specific picture of who their customers are and what they want and tailor customer experiences accordingly.

"Traditional players need to shift their perspective from being a fuel supply business to being a retail business that sells fuel"

This hyper attention to the customer experience is a hallmark of disruptors. Are disruptors jumping into this market today?

The fuel retail market is a mature industry, and I imagine that new players will want in because there is less competition at this stage. We’re seeing this pattern in upstream right now.

For example, multinationals have sold their assets in the North Sea basin to independents, new entrants, and national oil companies. With agile teams, different business mindsets, and new technologies, these disruptors are exploring with subsea pumping technology. As downstream reaches the end of its maturity lifecycle, new entrants are bound to set their sights on this market as well.

“The trick for the industry is to use data to get a very specific picture of who their customers are”

Who do you think the disruptors will be in downstream markets in France?

One of the first bets I would place would be on a national oil company. Saudi Aramco, the Saudi Arabian national oil company, and Total are working together in a joint venture to modernize fuel stations in Saudi Arabia. They could propose deploying this model in other geographies to expand their geographic footprint. We could also see consolidation among dealers to purchase more stations moving the center of gravity towards the Dealer Owned-Dealer Operated (DODO) operating model.

There’s something interesting we are already seeing in France. To encourage people to take the highway—and pay tolls—toll operators have started owning stations. This is relevant only to fuel stations on the highway, which is about 10 percent of those in the country. But this is still a disruptive play putting pressure on the only captive market where fuel prices are relatively higher and so are wet product margins.

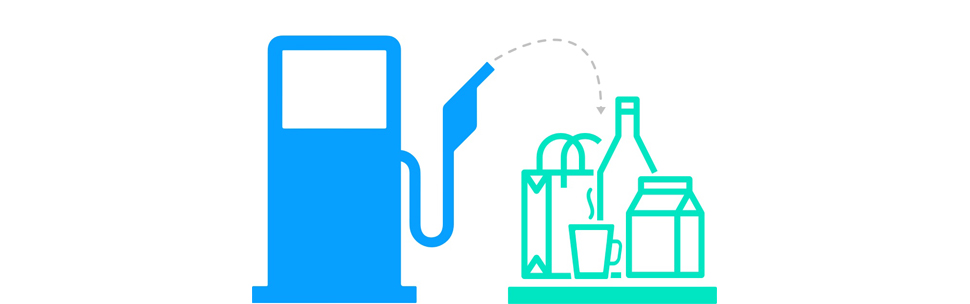

Do you envision a time when gas isn’t what draws consumers to the fuel station?

We have done some thinking on this topic by imagining the personas of consumers visiting fuel stations. There are three profiles to consider—the daily commuter, the family and the long-haul commuter. Their unique needs dictate why they visit the fuel station. The daily commuter wants to gas and go. So I think fueling up will always be the first draw. But families and long-haul commuters are more apt to be interested in retail products and services. But only if the industry can deliver exceptional experiences.

How can fuel stations of the future leverage their real estate footprint?

Fuel stations of the future are retail networks with a captive audience, a dynamic that’s ideal for advertising. Imagine the fuel station as a showroom. It could become a convenient destination to check out the latest model of a luxury car or the spring line of designer clothes. The more consumer data the industry harvests, the better positioned they are to work with partners to develop highly targeted experiences that reflect customer behaviors and purchasing patterns specific to different regions.

At Pilot Flying J – the largest travel center network in North America – we developed an app to save drivers time and money. It tailors the rest stop experience to drivers’ type of travel, location, preferences and needs. The app zeroes in on those key moments for its customers. For example, it can recognize when professional drivers arrive on a property and can deploy time-saving features like mobile fueling, shower reservations and saved offers.

It is 2025. You pull into a fuel station. What is the biggest difference from today? What is the most surprising change?

Here’s what the experience looks like. I’ve got the mobile app downloaded on my phone. I pull into the station; my car is immediately recognized through license place recognition. I get a welcome and some targeted deals aligned to my preferences and purchasing history. I pay via the app, and that’s it. No queuing at the pumps, and no queuing in the retail store. It’s a seamless experience, like Amazon Go.

I think the biggest difference in all of this is the amount of control that the consumer has over the experience. And I think the biggest surprise is that all of the enabling technology is mature today and being used now in other industries, especially retail. These concepts are not futuristic, horizon concepts like parking a car on a car pad that rotates it through servicing. Without massive R&D investment, industry players can deliver more value and make a business going through immense change more profitable—even at this later phase of maturity. And what makes this investment compelling is that it will increase the attractivity of the retail network. Whether oil companies are planning to harvest or to divest, they are better off with an attractive retail business.